By The Greensboro Chronicle |

Legal Disclaimer: This article is informational in nature and does not constitute legal, financial, or immigration advice. Readers should consult qualified attorneys or financial professionals before making business or immigration decisions. |

© 2026 The Greensboro Chronicle. All rights reserved.

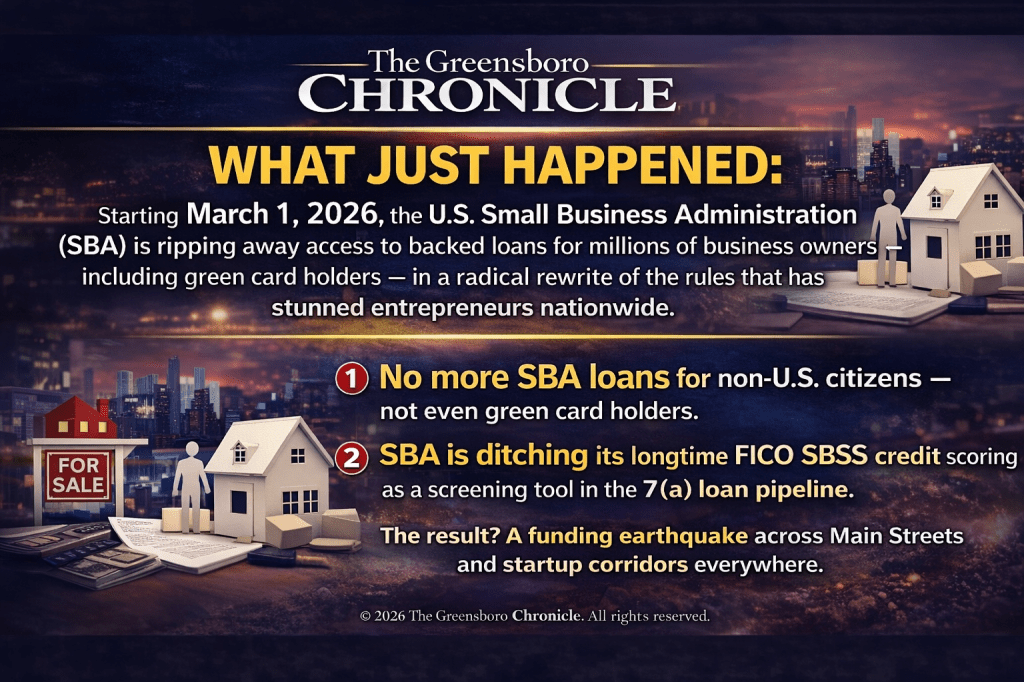

🔥 What Just Happened:

Starting March 1, 2026, the U.S. Small Business Administration (SBA) is ripping away access to backed loans for millions of business owners — including green card holders — in a radical rewrite of the rules that has stunned entrepreneurs nationwide.

These changes include:

1. No more SBA loans for non-U.S. citizens — not even green card holders.

2. SBA is ditching its longtime FICO SBSS credit scoring as a screening tool in the 7(a) loan pipeline.

The result? A funding earthquake across Main Streets and startup corridors everywhere.

🧠 What Used to Be — The Old SBA Rules

For decades, SBA loans were America’s secret sauce for small business financing: affordable terms, partial federal guarantees, and lifelines for startups that couldn’t get conventional bank capital.

Before March 2026, the basic eligibility landscape looked like this:

✔️ Businesses could receive SBA 7(a) and 504 loans if they were located in the U.S. and met size and credit standards.

✔️ Owners had to be U.S. citizens or lawful permanent residents (green card holders) — but minority non-citizen ownership was often allowed up to specific thresholds.

✔️ SBA used the FICO Small Business Scoring System (SBSS) to pre-screen many 7(a) applications through a credit score range (0–300).

Non-citizens, including conditional residents or certain visa holders, could sometimes qualify or apply through nuanced lender discretion and specific documentation — though this was always complex.

⚠️ WHAT TRIGGERED THIS EARTHQUAKE CHANGE

🎯 Policy Overhaul and Executive Pressure

The SBA’s drastic rewrite is tied to broader federal policy shifts aimed at tightening citizenship verification in federal benefits — including loan programs — under recent executive directives and internal SBA policy notices. These directives expanded the definition of ineligible persons to include many non-citizens in managerial or ownership roles.

📉 Stricter Risk Controls and Political Blame Games

Officials pitched these changes as “protecting taxpayers” and aligning eligibility with stringent immigration enforcement priorities. Critics — including bipartisan lawmakers — argue that these rules have unintentionally strangled small business lending, contributing to sharp drops in approvals and blocking financing for vibrant immigrant entrepreneur communities.

🚨 NEW DEADLY RULES FOR SBA LOANS, EFFECTIVE MARCH 1, 2026

❌ No Non-Citizens — Even Green Card Holders

Effective March 1, 2026:

👉 If any direct or indirect owner of a business is not a U.S. citizen or U.S. national with permanent residency, the business cannot borrow SBA loans — period. Green card holders are explicitly stripped of eligibility.

Previous exceptions allowing up to 5% ownership by non-citizens have been rescinded.

🚫 FICO SBSS Credit Screening Dropped

In a parallel move, SBA will no longer use the FICO SBSS score to screen 7(a) applications — meaning:

📉 The standardized, semi-predictive scoring that helped lenders assess business credit risk is gone.

📉 Lenders must now rely more heavily on manual underwriting, cash-flow analyses, and other subjective factors.

This adds new friction — and uncertainty — to lending decisions.

🧍♂️ WHO THIS HITS THE HARDEST

Non-Citizens

🌎 Immigrant entrepreneurs, startup founders, and family businesses that depend on SBA backing are suddenly locked out — even if they’ve lived, worked, and paid taxes for years.

Small Businesses With Non-U.S. Managers

Changes in ownership and key employee definitions could even disqualify companies where *owners are citizens but key employees are not — a controversial interpretation that critics say goes beyond citizenship intent.

Lenders and Local Economies

Banks and credit unions must now rewrite underwriting procedures — at a time of stagnating small business credit — potentially worsening the lending drought.

💡 ARE THERE STILL PATHS FOR NON-CITIZENS?

It’s not all shutdowns — but options are limited, complex, and often higher-cost:

✔️ Alternative Lenders

Private small business lenders, community development financial institutions (CDFIs), or microloan programs that do not depend on SBA guarantees might still work with lawful non-citizens.

✔️ State & Local Grants

Some states and municipalities offer grant programs irrespective of federal citizenship eligibility.

✔️ Immigrant-Focused Funds

Certain nonprofit and angel investment funds focus on immigrant business owners — but these are not SBA guarantees and often require pitch quality & collateral.

✔️ Visa-Linked Funding

EB-5 and certain investor visa categories can open doors to capital inflows, but are costly and require complex immigration/legal planning.

📢 CALL TO ACTION — URGENT AND BOLD

Small business owners across the U.S., regardless of citizenship status, cannot afford delay.

If you are a business owner or investor who:

✔️ Has an SBA loan pending

✔️ Wants capital for growth

✔️ Has immigrant co-owners or managers

✔️ Relies on SBA 7(a) or 504 financing

You MUST ACT NOW.

🔎 Talk to a qualified SBA lender immediately to assess your current application before March 1, 2026.

📞 Consult an immigration attorney to explore whether your status or ownership structure can be preserved under the new rules.

📈 Seek alternative financing channels — sooner, not later.

The American Dream has never been this precarious. Act before your future is legislated away.

Copyrights © 2026 The Greensboro Chronicle. All rights reserved. Reproduction in whole or part without permission is prohibited.