DriveTime & Bridgecrest Under Scrutiny

An Investigative Look at Alleged Online Payment Fee Violations and Mass Arbitration Efforts

A growing wave of consumer complaints and legal scrutiny is placing DriveTime and its affiliated auto-loan servicer Bridgecrest under the microscope. Attorneys investigating the companies’ online payment practices allege that borrowers may have been charged undisclosed or inadequately disclosed convenience fees when making loan payments through Bridgecrest’s online portal—potentially violating state and federal lending and debt-collection laws.

Now, law firms are organizing mass arbitration claims on behalf of affected borrowers. If you made an online payment through Bridgecrest within the past 12 months, your claim could be worth hundreds of dollars.

The DriveTime–Bridgecrest Relationship

DriveTime operates as one of the nation’s largest buy-here-pay-here-style used vehicle retailers, targeting consumers with limited or damaged credit histories. Most DriveTime customers do not receive traditional third-party auto loans. Instead, their financing is commonly serviced by Bridgecrest, a related entity that manages billing, payments, and collections.

This vertical integration—vehicle sales, financing, and loan servicing under one corporate umbrella—has long raised concerns among consumer advocates about transparency, leverage over borrowers, and fee practices.

What Borrowers Are Alleging

At the center of the emerging legal action is a deceptively small line item: online payment fees.

Borrowers allege that when making payments through Bridgecrest’s online portal:

Fees were added at checkout without clear advance disclosure The fees were framed as optional or unavoidable without offering a fee-free alternative that was equally accessible Disclosures were buried in fine print, vague language, or post-login screens Consumers were not clearly informed whether fees went to Bridgecrest, a third-party processor, or both

In many cases, borrowers report discovering the fee only after completing the transaction, leaving them with no realistic opportunity to avoid it.

Why This May Be Illegal

Legal experts point to several consumer-protection laws that may be implicated:

1. Truth in Lending Act (TILA)

TILA requires lenders and servicers to clearly and conspicuously disclose all finance charges connected to a loan. If online payment fees are effectively mandatory or routinely incurred, they may qualify as finance charges requiring upfront disclosure.

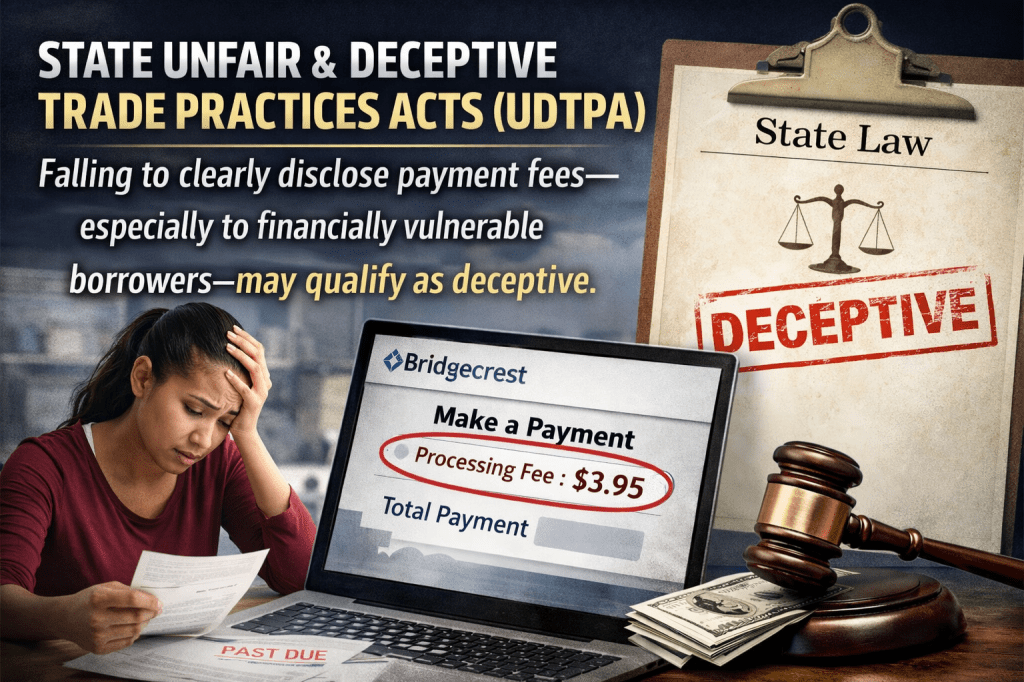

2. State Unfair and Deceptive Trade Practices Acts (UDTPA)

Most states prohibit business practices that mislead consumers or omit material information. Failing to clearly disclose payment fees—especially to financially vulnerable borrowers—may qualify as deceptive.

3. Fair Debt Collection Practices Act (FDCPA)

While typically applied to third-party collectors, courts have increasingly scrutinized servicing practices that add unauthorized fees or misrepresent amounts owed.

4. Electronic Fund Transfer Act (EFTA)

EFTA governs electronic payments and prohibits conditioning payments on fees unless certain disclosures and alternatives are provided.

Why Mass Arbitration Is Being Used

Rather than filing a traditional class-action lawsuit, attorneys are pursuing mass arbitration—a strategy increasingly used when companies include arbitration clauses in consumer contracts.

Under this approach:

Each borrower files an individual arbitration claim Companies must pay filing and administrative fees for each case When hundreds or thousands of claims are filed simultaneously, costs can escalate rapidly

This strategy has proven effective in forcing large corporations to settle claims or reform practices, even when class actions are contractually restricted.

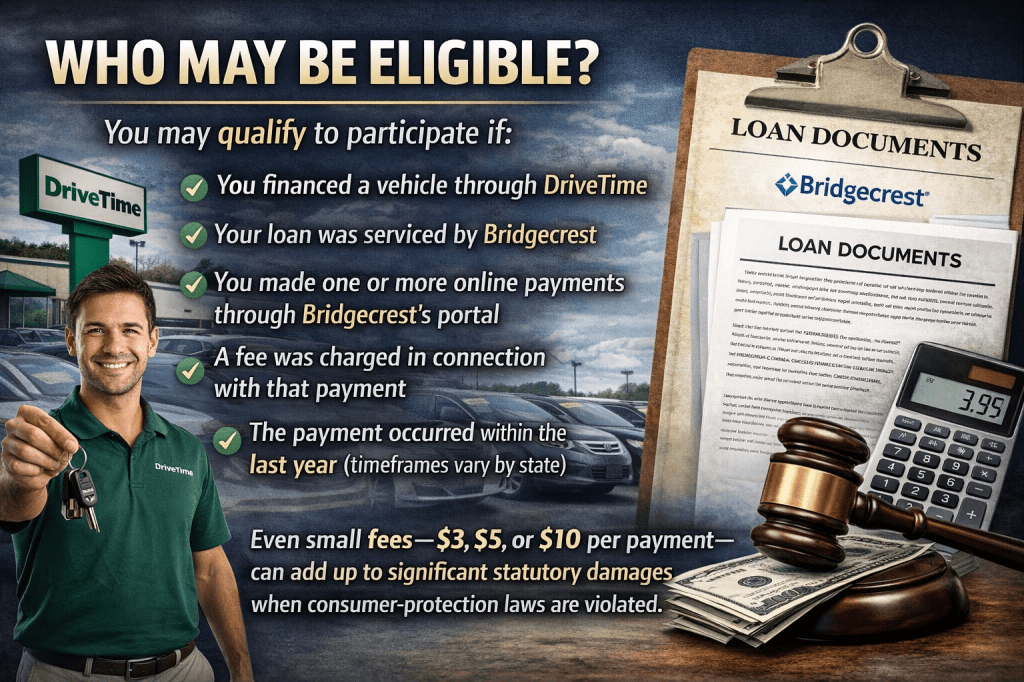

Who May Be Eligible

You may qualify to participate if:

You financed a vehicle through DriveTime Your loan was serviced by Bridgecrest You made one or more online payments through Bridgecrest’s portal A fee was charged in connection with that payment The payment occurred within the last year (timeframes vary by state)

Even small fees—$3, $5, or $10 per payment—can add up to significant statutory damages when consumer-protection laws are violated.

Potential Compensation

While outcomes vary, attorneys involved in similar cases report that successful claims may result in:

Refunds of all fees paid Statutory damages under consumer-protection laws Settlement payments ranging from tens to hundreds of dollars per borrower Policy changes requiring clearer disclosures or fee elimination

Importantly, participation in mass arbitration typically does not require upfront legal fees for borrowers.

The Bigger Picture: Subprime Auto Lending Under Fire

This investigation fits into a broader national reckoning over subprime auto lending, where consumers with few alternatives are often subjected to:

Aggressive fee structures Limited payment options High-interest rates paired with add-on charges Opaque servicing practices

Regulators, including the Consumer Financial Protection Bureau, have repeatedly warned that digital payment platforms are not exempt from disclosure requirements simply because transactions occur online.

What Borrowers Should Do Now

If you believe you were affected:

Review your payment history and look for “convenience,” “processing,” or “online payment” fees Save screenshots or statements showing the fees Document how and when the fee was disclosed (if at all) Monitor announcements from consumer-rights law firms gathering DriveTime/Bridgecrest borrowers

Why This Investigation Matters

For many borrowers, a few dollars per payment may not seem worth challenging. But consumer advocates stress that systematic small fees, applied across tens of thousands of accounts, can generate millions in revenue—often extracted from consumers least able to absorb the cost.

If the allegations are proven, this case could force meaningful changes in how auto lenders disclose fees, design payment portals, and treat borrowers navigating already precarious financial situations.

The Greensboro Chronicle will continue monitoring this developing legal action and its implications for consumer rights nationwide.

Watch the full video on YouTube

Leave a comment